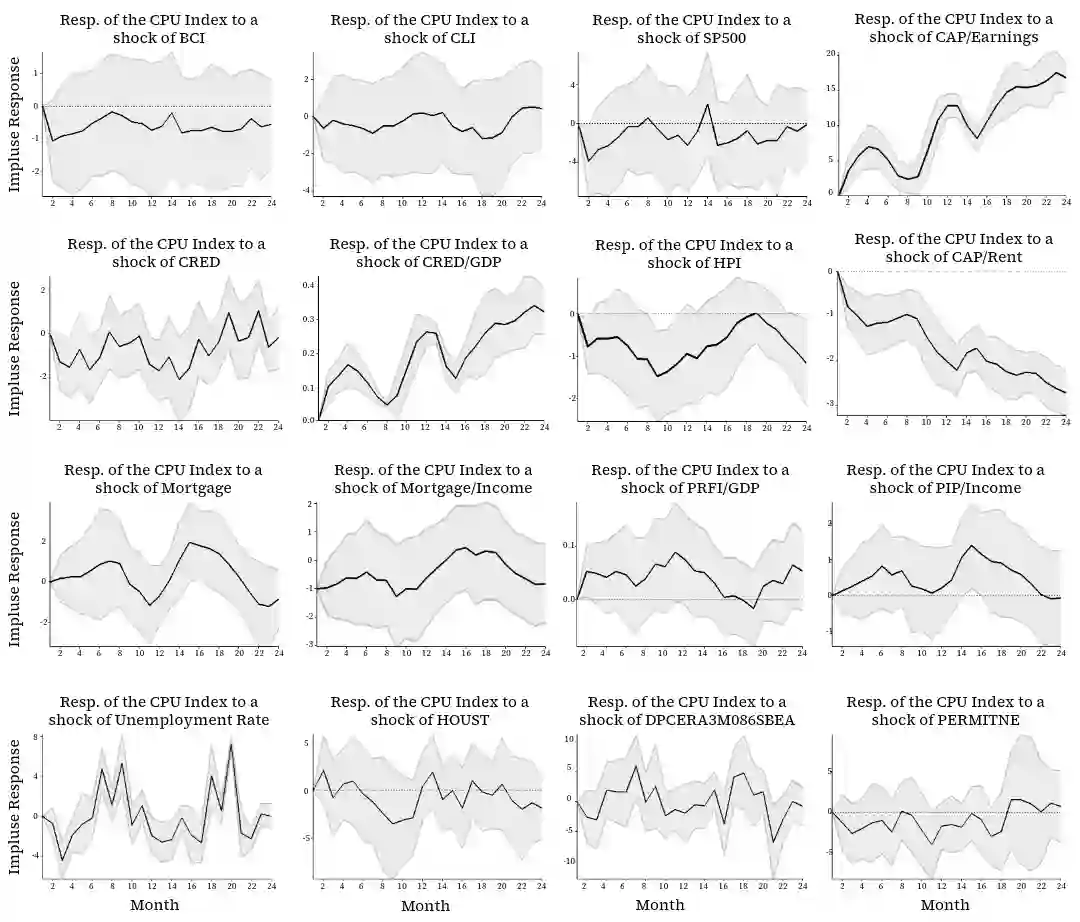

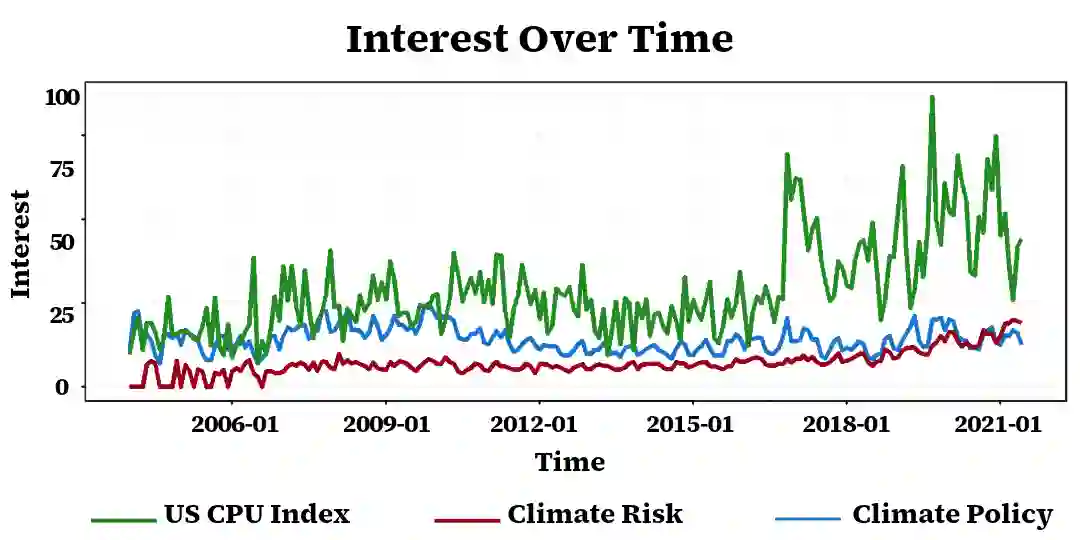

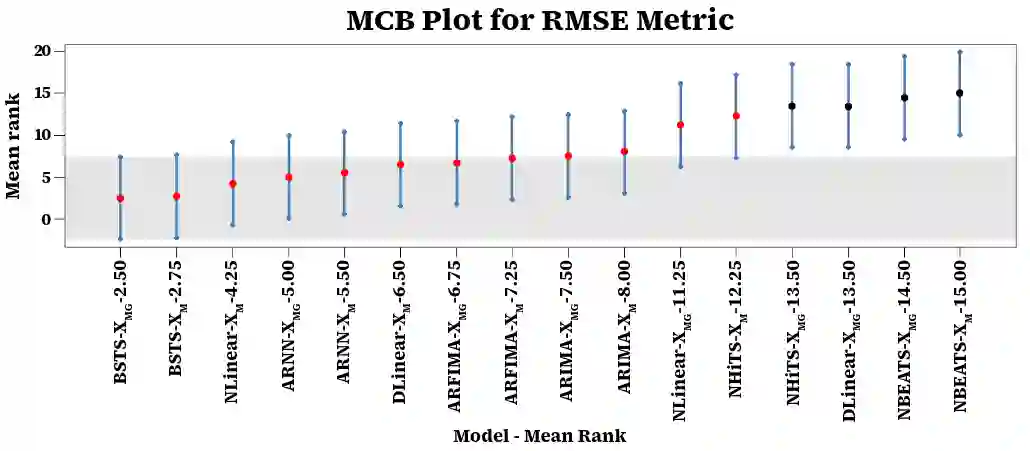

Accurately forecasting Climate Policy Uncertainty (CPU) is critical for designing effective climate strategies that balance economic growth with environmental objectives. Elevated CPU levels deter investment in green technologies, delay regulatory implementation, and amplify public resistance to policy reforms, particularly during economic stress. Despite the growing literature highlighting the economic relevance of CPU, the mechanisms through which macroeconomic and financial conditions influence its fluctuations remain insufficiently explored. This study addresses this gap by integrating four complementary causal inference techniques to identify statistically and economically significant determinants of the United States (US) CPU index. Impulse response analysis confirms their dynamic effects on CPU, highlighting the role of housing market activity, credit conditions, and financial market sentiment in shaping CPU fluctuations. The identified predictors, along with sentiment based Google Trends indicators, are incorporated into a Bayesian Structural Time Series (BSTS) framework for probabilistic forecasting. The inclusion of Google Trends data captures behavioral and attention based dynamics, leading to notable improvements in forecast accuracy. Numerical experiments demonstrate the superior performance of BSTS over state of the art classical and modern architectures for medium and long term forecasts, which are most relevant for climate policy implementation. The feature importance plot provides evidence that the spike-and-slab prior mechanism provides interpretable variable selection. The credible intervals quantify forecast uncertainty, thereby enhancing the model's transparency and policy relevance by enabling strategic decision making.

翻译:准确预测气候政策不确定性(CPU)对于设计有效的气候战略至关重要,这些战略旨在平衡经济增长与环境目标。CPU水平升高会阻碍绿色技术投资、延迟法规实施,并加剧公众对政策改革的抵制,尤其是在经济压力时期。尽管越来越多的文献强调了CPU的经济相关性,但宏观经济和金融条件如何影响其波动的机制仍未得到充分探讨。本研究通过整合四种互补的因果推断技术,识别了美国CPU指数在统计和经济上显著的决定因素,从而填补了这一空白。脉冲响应分析证实了这些因素对CPU的动态影响,突显了房地产市场活动、信贷条件和金融市场情绪在塑造CPU波动中的作用。所识别的预测因子,以及基于情绪的Google Trends指标,被纳入贝叶斯结构时间序列(BSTS)框架进行概率预测。引入Google Trends数据捕捉了基于行为和注意力的动态变化,显著提高了预测准确性。数值实验表明,在中期和长期预测中,BSTS优于最先进的经典和现代架构,这些预测对气候政策实施最为相关。特征重要性图证明,尖峰-平板先验机制提供了可解释的变量选择。可信区间量化了预测不确定性,从而通过支持战略决策制定,增强了模型的透明度和政策相关性。