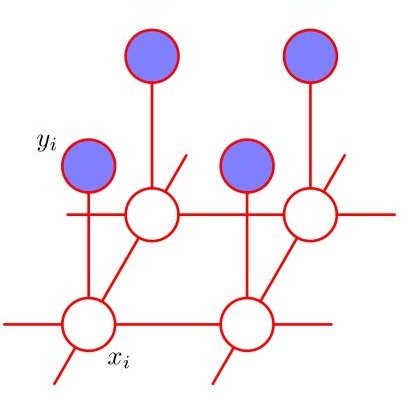

In many insurance contexts, dependence between risks of a portfolio may arise from their frequencies. We investigate a dependent risk model in which we assume the vector of count variables to be a tree-structured Markov random field with Poisson marginals. The tree structure translates into a wide variety of dependence schemes. We study the global risk of the portfolio and the risk allocation to all its constituents. We provide asymptotic results for portfolios defined on infinitely growing trees. To illustrate its flexibility and computational scalability to higher dimensions, we calibrate the risk model on real-world extreme rainfall data and perform a risk analysis.

翻译:暂无翻译

相关内容

ACM/IEEE第23届模型驱动工程语言和系统国际会议,是模型驱动软件和系统工程的首要会议系列,由ACM-SIGSOFT和IEEE-TCSE支持组织。自1998年以来,模型涵盖了建模的各个方面,从语言和方法到工具和应用程序。模特的参加者来自不同的背景,包括研究人员、学者、工程师和工业专业人士。MODELS 2019是一个论坛,参与者可以围绕建模和模型驱动的软件和系统交流前沿研究成果和创新实践经验。今年的版本将为建模社区提供进一步推进建模基础的机会,并在网络物理系统、嵌入式系统、社会技术系统、云计算、大数据、机器学习、安全、开源等新兴领域提出建模的创新应用以及可持续性。

官网链接:http://www.modelsconference.org/

专知会员服务

54+阅读 · 2020年1月30日

专知会员服务

34+阅读 · 2020年1月15日

专知会员服务

34+阅读 · 2019年10月18日

专知会员服务

36+阅读 · 2019年10月17日

相关VIP内容

专知会员服务

54+阅读 · 2020年1月30日

专知会员服务

34+阅读 · 2020年1月15日

专知会员服务

34+阅读 · 2019年10月18日

专知会员服务

36+阅读 · 2019年10月17日

相关资讯

相关论文